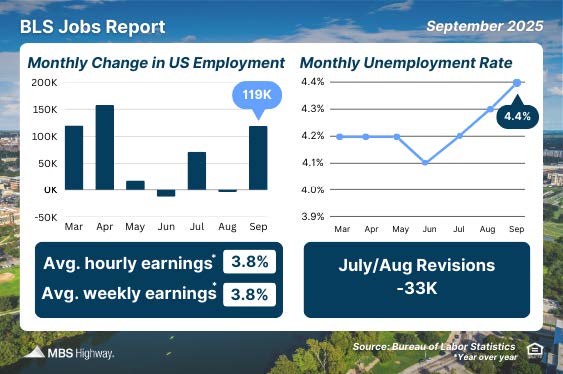

September job growth came in stronger than expected, with 119,000 jobs added versus the 50,000 forecast. However, revisions to July and August reduced the previous totals, leaving August with a net decline of 4,000 jobs. This follows a 13,000-job loss in June, marking the first two monthly declines since December 2020. The unemployment rate inched up from 4.3% to 4.4%.

What’s the bottom line?

Because of the government shutdown, this report was delayed – and the Bureau of Labor Statistics (BLS) will release only partial October data (without an unemployment rate) alongside the full November report on December 16.

That timing matters: it’s after the Fed’s next policy meeting on December 9-10. The Fed has already cut the Fed Funds Rate in both September and October as it tries to balance above target inflation with signs of labor market cooling.

After the October meeting, Chair Jerome Powell cautioned there is “no risk-free path” ahead and emphasized that another rate cut on December 10 “is not a foregone conclusion.” Meeting minutes showed significant debate and a majority leaning against a December cut, and recent Fed commentary has underscored this divide.

The Fed is weighing two competing goals: keeping inflation in check and supporting employment. High inflation typically argues against rate cuts, while weakening labor data can push policymakers toward easing.

With September’s mixed report – stronger-than-expected job growth but a rising unemployment rate – and no additional jobs reports arriving from the BLS before the December meeting, the likelihood of another rate cut remains uncertain.

Quick refresher: When the Fed adjusts rates, it changes the Federal Funds Rate – the short-term rate banks charge each other. This doesn’t directly set mortgage rates, but it influences them alongside broader economic conditions.