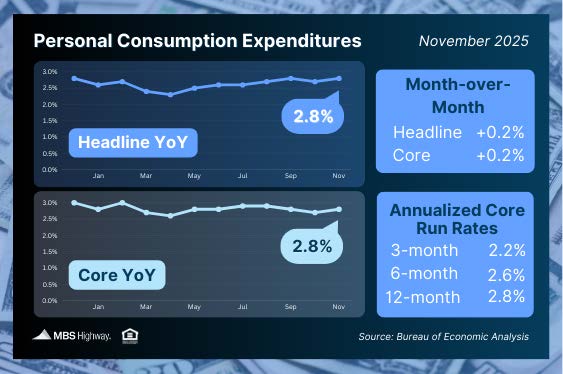

The government released the delayed Personal Consumption Expenditures (PCE) report for October and November, with results largely matching expectations. Headline and core inflation both rose 0.2% in each month, leaving the annual rate at 2.8%. Core PCE, which excludes food and energy, is the Federal Reserve’s preferred inflation measure.

What’s the bottom line?

The Fed continues to balance lingering inflation pressures against signs of a cooling labor market. Persistent inflation argues for caution on rate cuts, while softer employment data increases pressure to ease policy. The Fed lowered its benchmark Federal Funds Rate by 25 basis points three times last fall. While this rate does not directly determine mortgage rates, it influences borrowing costs across the broader economy.

Fed Chair Jerome Powell has emphasized that there is “no risk-free path,” highlighting that both inflation and labor market trends will shape policy decisions in the months ahead. Encouragingly, the monthly inflation readings for October (0.21%) and November (0.16%) were relatively low. Looking ahead, inflation progress could improve further if monthly readings remain subdued early this year. Higher readings from January and February 2025 (0.31% and 0.45%) will roll off the 12-month average, potentially making it easier to see faster progress toward the Fed’s 2% inflation target.